Credit: Nathan Burton/The New Mexican

I Saw the Sun(Zia)

SunZia, a 3.5 GW wind project development in New Mexico, just started operations – it’s now the largest renewables project in the country. That is good, although what makes this a really fun story is that portfolio company Grid Status noticed California was producing a lot more wind energy, dug into it, and figured out it was the new SunZia project testing its new turbines, so they are credited with the news scoop of the largest renewables project in the country turning on, despite not being reporters themselves (Ben Storrow at E&E News, a real reporter, subsequently wrote on the subject to highlight it as well).

This is a project that is based in New Mexico, but through the magic of transmission lines (HVDC in this case, which is essentially a giant extension cord), it is feeding into and being controlled by the California grid.

One slightly less less magical element of this project? It took 17 years for the permitting process to come together – I recall back when I was a young whippersnapper working on transmission development at the Department of Energy in 2012 and SunZia was already multiple years into the process of coordinating with and securing various federal approvals. Plenty of room for process improvement here!

Data centers and Off Grid Gas: How Much There There?

It’s 2026 so we can’t not talk about off grid data center project development. Microsoft is collaborating with Nscale in West Virginia on an off-grid gas project, for new data centers. I was a little surprised to see this (it’s Microsoft’s first off-grid gas project for data centers, although this is a project that’s been in the works for a couple of years and appears to have some unique factors working for it so presumably they have turbine supply locked down and can move quickly as a result).

More broadly, off-grid gas power for data center development is interesting not only for its implications for emissions and for how the grid evolves, but also because there is a wide band of uncertainty about what’s actually going to happen. Anywhere where smart thoughtful people are disagreeing significantly is an interesting area in my book.

The analysts at Cleanview charted how the off-grid data center development space has grown from nothing 18 months ago to around 30% of planned data center capacity, and possibly growing (overwhelmingly this is gas in the near term but more varied looking 5+ years out).

At the same time, industry stakeholders are suggesting that fewer off-grid data centers will actually get built than currently projected. Indeed, recent analysis suggests that overall, 40% of the data centers planned to be delivered this year haven’t begun construction yet (for all data centers, not just the off grid ones). In addition to challenges securing gas turbines, the chips themselves are in short supply as well, and local opposition will act as a headwind (to any data center project regardless of how it is powered). General operational experience and execution is likely a factor as well – recent analysis from Aurora Energy Research suggests that more than half of planned data center capacity is from developers with no operational track record.

What are we to make of this? It seems like it can both be the case that there will be many more off-grid data centers to come (and increase significantly on a percentage basis at least, since they are starting from nearly zero), but also that a great many of these projects will not come to fruition. Some of this is for relatively boring supply chain reasons (if you can’t get a turbine, you are not going to build the plant; if natural gas prices stay elevated, that is going to weaken the economics of the marginal project).

I tend to be a bit skeptical about how much off-grid data center development will actually happen – not because it can’t, but just because it is expensive and complicated: the microgrid and power electronics requirements to have an entirely off-grid load are non-trivial. Also, if you don’t have your supply chain lined up and are delayed until 2032 to get your turbines, it is not clear that is any better than just building a normal power project (and being delayed until 2032 to get interconnected). On the other hand, it is clearly a boom time for anyone who can provide data center power and being able to get up and running means many millions of dollars in revenue opportunity.

Electricity Data for the People

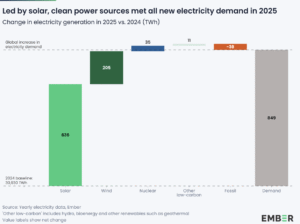

There are a couple of great new reports and tools related to electricity and energy. The first is Ember’s Global Electricity Review 2026, which is a new free dataset of global electricity generation in 2025.

Meanwhile, Heatmap recently collaborated with MIT an CleanEcon to develop a new tool, the Electricity Price Hub, to show what people actually pay for electricity in the United States.

The thing that stands out to me from the Ember report is how the American electricity landscape, which is acutely focused on speed to power for data centers, is very different from the global landscape, where the big story is how much solar is being built.

Some of the headlines from that report that resonated:

- Clean power met the global growth in electricity demand on net

- China and India (where the most fossil power growth is happening) both recorded a drop in fossil generation in 2025 as they added more renewables than demand grew

- In markets where solar and batteries are being rapidly adopted like Australia and Chile, enough storage was built in 2025 to shift more than half of new solar generation over the last year (if you can shift a lot of solar, you can really bring down the peak load, which allows you to have a system with much higher utilization, which is great economically, and also typically results in using less of the most polluting generators that only run during peaks)

Carbon Removal Hiccup?

Microsoft has in recent years been the largest purchaser of carbon removal in the world, accounting for 90% of all purchases last year. This year, it appears the company is halting new purchases for the time being (although they aren’t cancelling existing contracts) – this is likely to be a major hurdle for CDR companies getting to revenue. That said, as an investor in carbon removal startups, counting on one single customer as the basis for a go-to-market plan doesn’t really pass muster anyways (even if it was huge and sophisticated).

Other News

Walmart is rapidly expanding its high speed charging network. This is good in general, and extra fun because the effort is being spearheaded by a former Evergreen intern – way to go Olivia!

EIA shared a thorough rundown of all the different approaches to developing new nuclear rectors being pursued currently.

Great interactive here graphics about US electricity use from the New York Times and Robinson Meyer.

Tandem PV has launched a pilot manufacturing facility to produce sample tandem perovskite / silicon photovoltaic panels (perovskites have long been held up as an opportunity to make much more efficient panels, but have to overcome a number of commercialization challenges related to stability and durability as well).

Speaking of solar power innovation, Meta signed up for a gigawatt of solar from Overview Energy, which is trying to beam solar power from space (in their case, using existing solar installations as the receivers of that energy). While they were at it, Meta also signed up for a gigawatt of long duration storage (up to 100 hour duration) from Noon Energy.

After a big shift in US electric vehicle policy, automotive parts manufacturer Magna has a bunch of factories to build EV parts and not a lot of buyers.

Third Way shared an interesting report on where the advanced nuclear sector is today and how the government can best align incentives going forward.

PJM emergency generation auction yada yada yada.

Metal commodity trading business Trafigure signed a billion dollar offtake deal with battery materials refiner Nth Cycle.